The two candidates jostling to become the next prime minister of the United Kingdom are making big promises about rescuing the country’s economy. It won’t be an easy task.

Rishi Sunak and Liz Truss,two politicians for the country’s Conservative Party, are in the final running to replace Boris Johnson after his resignation earlier this month — and face an uphill struggle to revive an economy battling record inflation, anemic growth and labor shortages.

Starting last year, soaring energy prices and supply chain snarls have fueled global inflation as the world’s economies emerged from their pandemic lockdowns. Russia’s invasion of Ukraine in late February exacerbated the situation.

The country’s economic woes,though, run much deeper than the crises of the past two years. The UK economy is expected to stagnate next year, with zero growth in 2023 — the worst-expected performance in the G7, according to the Organisation for Economic Co-operation and Development.

Truss and Sunak have promised to tackle inflation to help households burdened by the worst cost-of-living crisis in decades. They both have said they will cut taxes — though on very different timescales — and reevaluate the UK’s relationship with its biggest trading partner, the European Union.

But Ethan Ilzetzki, associate professor of economics at the London School of Economics, thinks the leadership debate remains “disconnected” from the nature and scale of the economic challenges: A decade-long stagnation in productivity levels won’t be easily solved.

“None of them have a true plan except for cutting taxes,” he told CNN Business.

“It is all about the level of taxes, the size of government. These are important questions… [but] there is no easy fix in terms of slashing taxes to the deep problems we have here,” he said.

While some of the difficulties ailing the world’s fifth largest economy will largely be beyond either Sunak or Truss’ control, they have made bold promises to Britons. Can they deliver on them?

Global energy prices

Sunak, the government’s former finance minister, has said tackling inflation is his biggest priority — annual consumer price inflation in the UK hit another 40-year high last month to reach 9.4%. That’s the fastest increase among the G7 nations.

But Sunak’s options are limited, if not nonexistent, given how exposed the UK, as a major importer of fuel, is to global energy prices.

“We are importing that inflation,” Sanjay Raja, Deutsche Bank’s chief UK economist, told CNN Business.

The Bank of England has hiked interest rates five times since December in a bid to tame spiraling prices. It expects inflation to top 11% later this year. But its powers are limited, says Raja.

“The UK, as a small, open economy, can’t do very much, [it] can’t supply and make up these goods to limit the increase in prices to offset that inflation,” Raja said.

The country is spending more importing goods than it makes from its exports. Rocketing fuel costs have helped the UK rack up a trade deficit of 8.3%, the largest since the government’s statistics office started keeping records in 1955.

Add to that a weakened currency — the pound has lost nearly 12% of its value against the US dollar since the start of this year — and the country can expect the costs of its imports to increase, while its exports could become more competitive on the global market.

“There’s a lot more money going out than coming in,” Maria Demertzis, interim director at Bruegel, an economics think tank, told CNN Business.

The UK has effectively dipped into its savings, Demertzis said, to help it absorb the shocks of the past few months. This is only a problem if it continues for much longer.

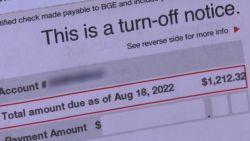

But global energy prices show little sign of cooling in the near term. Eye-watering wholesale natural gas costs have pushed up the annual energy bill for millions of UK households by 54% this year. Bills are expected to climb again in the fall to top £3,000 ($3,572), according to energy research firm Cornwall Insight.

Britons have tightened their belts in response, spending less in supermarkets and ditching their streaming subscriptions.

Indeed, real pay — workers’ wages that take inflation into account — suffered its biggest drop in more than two decades between March and May, official data showed this week.

To tax or not to tax

Truss is hoping to offer workers and businesses a lifeline, promising to slash income taxes and scrap a planned tax hike on businesses next year. But increased spending could exacerbate inflation and undermine the Bank of England’s efforts to slow down the economy to tame runaway price increases.

Sunak has also promised to cut taxes but only once inflation is brought under control.

The Institute for Fiscal Studies (IFS) has estimated that Truss’ total tax cuts would amount to £30 billion ($36 billion). She has not laid out any plans to rein in public spending to compensate for a drop in tax receipts.

It’s an appealing message for the millions struggling to make ends meet, but her critics say the moves would further fuel inflation and increase public debt, which is on track to hit £100 billion this year.

In June, inflation pushed up public debt interest payments to the highest level since the government started keeping records 25 years ago.

“Certainly [cutting income tax] would strengthen incentives to enter work and to earn more, though these effects would not be nearly sufficient to make the reform pay for itself,” the IFS said in a Thursday note.

If Truss wins and fails to cut spending, the IFS said, reality would ultimately bite. “But in the end lower taxes do mean lower [public] spending,” it added.

Productivity slump

Despite a small lift to the UK’s GDP in May, the last month for which there is data, fears that the country will tip into a recession have not gone away.

Yet one of the biggest drivers of growth — productivity — has stagnated since the financial crisis in 2008.

“The heart of economic growth lies in productivity growth,” Dean Turner, European and UK economist at UBS bank, told CNN Business. Productivity measures the output per unit of capital, labor or other inputs.

According to the the Office for National Statistics, in the decade to 2007, the UK’s output per hour of work grew by 1.9% on average each year, but fell to 0.7% in the decade after the financial crisis. That’s the second-slowest growth in the G7 after Italy.

Turner said that the UK would need to “rethink [its] whole economic model” to boost productivity.

“The fact of the matter is we just don’t do enough investment, we don’t do enough R&D in the UK, and that is something that’s hampering our productivity growth,” said Turner.

Higher productivity would be a boon for workers. Companies could produce more for the same number of staff, and afford to pay them higher wages.

Despite high inflation, average wages are no higher today that they were before 2008, the Resolution Foundation said in a report this month.

Ilzetzki said more investment in innovation, research and development, and providing job training to the labor force would go some way to boosting productivity, as well as encouraging immigration.

Yet not one of Truss and Sunak’s proposals would “put even a minor dent into the deep structural challenges that the UK faces,” he said.

Brexit still unresolved

According to Ilzetzki, a major priority for the next prime minister should be to clarify “once and for all, the UK’s relationship with its larger trading partner,” the European Union.

Truss, who voted to remain in the EU in 2016, has since become a staunch advocate for Brexit. She is pushing to rip up the Northern Ireland protocol — a piece of legislation central to the EU withdrawal agreement the UK signed in 2020 — which enables the free flow of goods between Northern Ireland and the Republic of Ireland.

The protocol keeps Northern Ireland subject to EU rules on internal trade, and means that goods traveling between the country and the rest of the UK must be checked.

Critics argue that the arrangement effectively creates a sea border within the UK, and involves burdensome costs and paperwork for businesses.

Truss, while serving as the UK’s foreign minister earlier this year, put forward legislation that promised to “end the untenable situation where people in Northern Ireland are treated differently to the rest of the United Kingdom,” and protect the country’s “territorial integrity.”

But overriding the protocol could lead to retaliation from the EU, with tariffs imposed on UK exports. The resulting trade war would be very bad for UK business.

Sunak has been less forthcoming on how he would handle the issue, but has previously said he would prefer to have a negotiated settlement with Europe.

The uncertainty is discouraging investment in the UK, Ilzetzki said.

“Nobody is going to invest in the UK for a few lower points of taxation when they aren’t certain whether UK exporters will be in a trade war with the EU within a year,” he added.

The twin impact of Brexit and the pandemic has also made it much harder for UK employers to tap a huge source of workers to help fill a grinding labor shortage.

Since January 2021, all EU nationals seeking work must pass through the same points-based immigration process as other nationalities. About 211,000 fewer EU nationals were working in the UK in the first quarter compared to the same period in 2020, while the number of non-EU workers rose by 182,000, according to official statistics.

To make matters worse, one million workers have exited the labor force, and many are unlikely to return. About half cited chronic ill health as the reason for leaving work, according to the Learning and Work Institute.

“We’ve seen an exodus of workers unlike anywhere else that we’ve seen in the advanced world,” Raja said.