Editor’s Note: Jeff Yang is a columnist for The Wall Street Journal Online and contributes frequently to radio shows, including Public Radio International’s “The Takeaway” and WNYC’s “The Brian Lehrer Show.” He is the co-author of “I Am Jackie Chan: My Life in Action” and editor of the graphic novel anthologies “Secret Identities” and “Shattered.” The opinions expressed in this commentary are solely those of the author.

Story highlights

On Monday, an 11-year-old Tennessee boy allegedly shot and killed an 8-year-old girl with his father's gun

Jeff Yang: Getting the insurance industry involved could be a great way to get meaningful gun reform

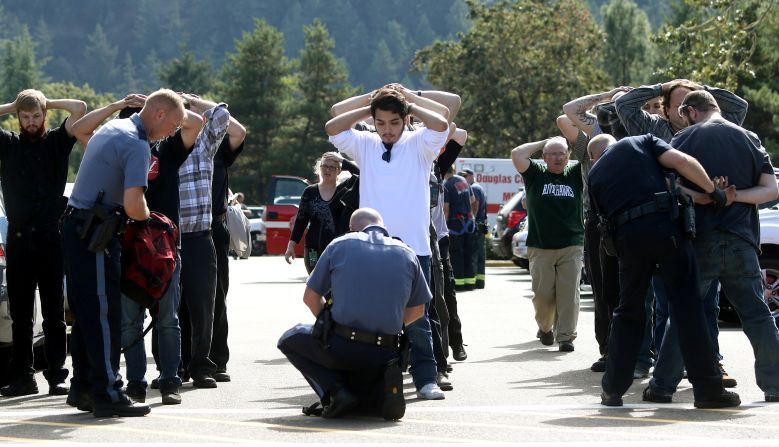

President Obama said it best: Our reaction to gun massacres has become a routine. It was only a week ago when a gunman killed nine people at Umpqua Community College in Oregon. And yet, the tragedy seems like it has already faded into the distant past.

Sure, right after the shooting, there was an all-hands-on-deck media scrum to report the horrible news. On social media, people were outraged. As always, there were assertions from gun-reform advocates that the crime could have been prevented if just maybe it was a little bit harder to obtain firearms in this country. As always, there was vehement pushback by Big Gun, declaring that guns are the cure to gun violence, not the cause, that any action to regulate them is tantamount to fascism, and that mental illness or lack of security are to blame for the bloodshed.

And then, a few days later, attention moved on to the next media distraction: The latest Kardashian antic, the latest celebrity in rehab, the latest cute animal video.

Discussions about basic and common-sense changes in the way guns are sold, secured and deployed in this country ground once more to a halt – until next time. But the period between “next times” continues to dwindle. And with each new tragedy it’s become clearer that the arguments being utilized by gun-reform advocates are effectively doomed, falling on hard hearts and deaf ears.

Why we’re still debating guns in 2015

On Monday, an 11-year-old Tennessee boy allegedly shot and killed an 8-year-old girl with his father’s 12-gauge shotgun because she wouldn’t let him play with his puppy. As is all too common with firearms incidents related to children, the gun had reportedly been left in an unlocked closet.

And this points the way to an uncomfortable truth about the current strategies used by those seeking reform of lax gun laws.

They’re nearly all focused on weapons and users, which makes it easy for the debate to be framed as being about “restriction” and “stripping away rights,” when the most powerful motivator for smart, practical regulation of firearms is the protection of victims.

Rethinking gun reform from the victim’s perspective not only changes the rhetoric drastically, it also surfaces a powerful hidden ally; one that has been demonstrably effective in helping to enact game-changing legislation in the past despite hysterical, implacable opposition.

The battle over gun policy: Old fight, new strategies

That ally is the insurance industry, whose support of Obamacare made all the difference in giving Americans sweeping access to health care for the first time in our nation’s history. Without the insurance industry’s lobbying, public advocacy and acceptance of disruptive change, Obamacare would have failed like every other attempt to reform our disastrous and doomed health care system.

Yes, the payback for the industry’s support of the legislation was significant; unlike most other developed markets in the world, the U.S. has wedded itself to the extraneous costs and chaotic volatility of private, for-profit insurance providers. But given the entrenched, death-before-compromise positioning of the political right, it’s clear that no real alternative existed to this market-based structure.

The same is true for gun reform. It is impossible to imagine a scenario tragic and ghastly enough for the American political system to proactively adopt a wise and pragmatic regulation of firearms. (If the killing of 20 elementary students in Sandy Hook didn’t sway gun-loving hearts and minds, nothing ever will.) The only recourse is to find a way to provide for the casualties of our national gun fetish.

Legislation that requires mandatory insurance for gun ownership – liability protection parallel to that required for use and operation of every other dangerous object in our society, from motor vehicles to heavy industrial equipment – is the answer to that need, giving victims of accident or intentional mayhem compensation for injury (and survivors, for loss of life), as well as a way to cover hospital bills and rehabilitation, and as is too often the case, funeral costs.

From a reform advocate’s perspective, getting the insurance industry on the side of sensible gun reform would transform both the narrative of the fight and the resources available to wage it. It means accepting the role of guns in American society, grimly and with heavy heart, but working with determination to ameliorate their impact.

It means making something of a devil’s bargain with a business category that’s focused on profitability and stock price rather than lost lives and grieving families. But desperate circumstances make for strange bedfellows, and having the megaphone and deep pockets of insurers on the side of reform would make a critical difference.

A legislative foothold already exists for this strategic shift. Earlier this year, U.S. Rep. Carolyn Maloney of New York introduced what she calls the Firearm Risk Protection Act, requiring liability insurance coverage for those seeking to purchase a weapon (with military service members and law enforcement officers exempted), and imposing a fine of $10,000 on those who fail to do so. As Maloney pointed out in a statement, “We require insurance to own a car, but no such requirement exists for guns. The results are clear: car fatalities have declined by 25% in the last decade, but gun fatalities continue to rise.”

The reason for the decline in car-related deaths: Auto insurers actively incentivize drivers to behave more safely – reducing their policy costs for avoiding speeding and reckless operation, and for having vehicles that are practical, properly maintained and safely secured.

It’s a market-based way to ensure that firearms owners embrace the duty of ownership along with the right, while also providing compensation for those who are harmed by gun-related accident and abuse. And it’s a strategy that the NRA might find some challenges responding to, given that they already offer liability insurance as a service to their members.

The claim that as many people die from cars as firearms each year is one of the most common pieces of rhetoric used by gun advocates to distract from the nation’s epidemic of gun-related harm.

It’s time for reformers to swallow hard, link arms with the insurance industry and take gun lovers at their word. If cars and guns are equally dangerous, let’s treat them in similar fashion – and ensure that victims across the country, from college students to puppy-loving 8-year-olds, have adequate recourse when they’re misused.